NTARE Spirit

May 19, 2025 at 07:13 AM

🪙 Here are some budget hacks to help you save money:

1. Track Your Expenses

Keeping track of where your money is going is crucial to saving. Write down every purchase, no matter how small, in a notebook or use an app like Mint.

2. Create a Budget Plan

Make a budget plan that accounts for all your necessary expenses, such as rent, utilities, and groceries. You can then identify areas where you can cut back.

3. Cut Back on Subscriptions

Review your subscriptions, such as streaming services, gym memberships, and magazine subscriptions. Cancel any that you don't use regularly.

4. Cook at Home

Eating out can be expensive. Cooking at home can save you around $5-10 per meal. Try meal planning and batch cooking to make the most of your groceries.

5. Avoid Impulse Buys

Make a shopping list and stick to it. Avoid buying things on impulse, especially if they're not on sale.

6. Shop Secondhand

Consider shopping at thrift stores, garage sales, or online marketplaces for secondhand items. You can often find great deals on gently used items.

7. Use Cashback Apps

Use cashback apps like Ibotta, Fetch Rewards, or Rakuten to earn money back on your purchases.

8. Save Your Change

Save your loose change in a jar or piggy bank. It may not seem like much, but it can add up over time.

9. Use the 50/30/20 Rule

Allocate 50% of your income towards necessary expenses, 30% towards discretionary spending, and 20% towards saving and debt repayment.

10. Avoid Fees

Be mindful of fees associated with bank accounts, credit cards, and other services. Avoid them whenever possible to save money.

11. Shop During Sales

Plan your shopping trips during sales periods, especially for non-perishable items. Stock up on items you use regularly.

12. Use Energy-Efficient Appliances

Using energy-efficient appliances can help reduce your utility bills. Look for appliances with the ENERGY STAR label.

13. Cancel Credit Card Interest

If you have credit card debt, consider consolidating it to a lower-interest card or balance transfer offer.

14. Use Public Transportation

Using public transportation, walking, or biking can save you money on fuel, parking, and vehicle maintenance.

15. Save on Entertainment

Look for free or low-cost entertainment options, such as hiking, game nights, or streaming movies instead of going to the theater.

By implementing these budget hacks, you can save money and achieve your financial goals.

🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹

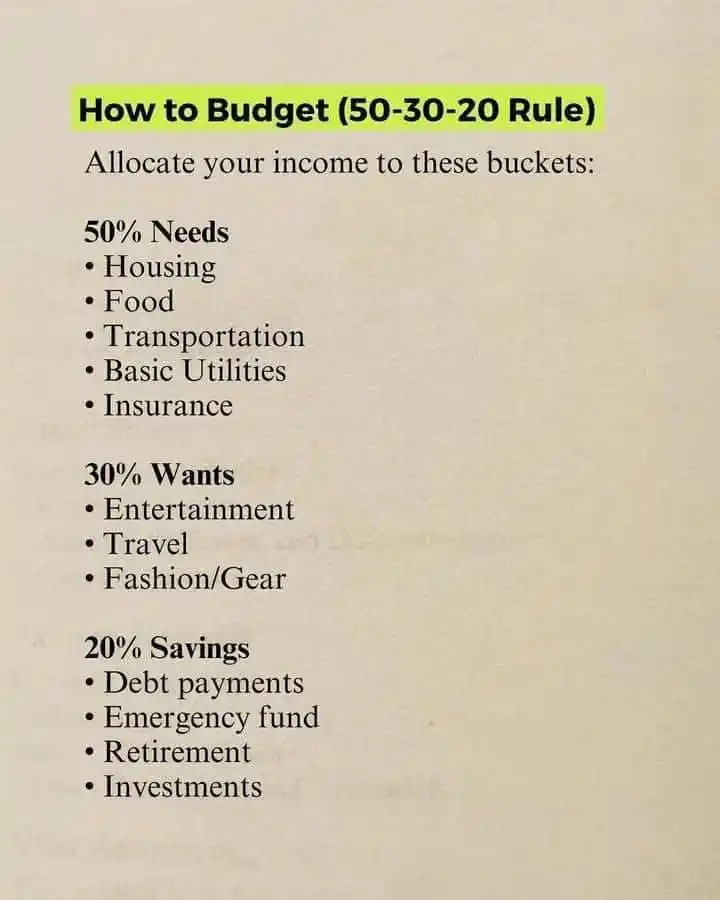

The 50-30-20 rule is a simple yet powerful budgeting framework that helps you allocate your after-tax income across three main categories: Needs (50%), Wants (30%), and Savings/Debt Repayment (20%). Let's break this down in much greater detail with practical examples.

Understanding Your After-Tax Income

First, you need to calculate your monthly take-home pay (after taxes and deductions). For example:

If your gross salary is $5,000/month

After 20% in taxes and deductions ($1,000)

Your take-home pay is $4,000

This $4,000 would then be divided according to the 50-30-20 rule.

50% for Needs ($2,000 in our example)

Needs are expenses you must pay to live and function in society. These are non-negotiable essentials:

Housing (30-35% of Needs)

Rent or mortgage payments

Property taxes

Homeowners/Renters insurance

Basic maintenance

Example: $1,000/month for rent (25% of take-home pay)

Food (15-20% of Needs)

Groceries

Basic household supplies

Example: $400/month for groceries and household items

Transportation (10-15% of Needs)

Car payments (if necessary for work)

Gas

Public transit costs

Basic maintenance/repairs

Example: $300/month for car payment, gas, and insurance

Utilities (10% of Needs)

Electricity

Water

Gas

Internet (basic plan)

Cell phone (basic plan)

Example: $200/month for all utilities

Insurance (5-10% of Needs)

Health insurance

Auto insurance

Disability insurance

Example: $100/month for health insurance premiums

Total Needs: $2,000 (50% of $4,000 take-home pay)

30% for Wants ($1,200 in our example)

Wants are discretionary expenses that enhance your lifestyle but aren't essential for survival:

Entertainment (25% of Wants)

Streaming services

Dining out

Movies/concerts

Hobbies

Example: $300/month (Netflix $15, dining out $200, hobbies $85)

Travel (20% of Wants)

Weekend getaways

Vacation savings

Example: $240/month set aside for annual vacation fund

Fashion/Gear (15% of Wants)

Clothing beyond basics

Electronics

Home decor

Example: $180/month for occasional clothing purchases

Personal Care (10% of Wants)

Salon visits

Spa treatments

Gym memberships

Example: $120/month for gym and occasional haircuts

Other Luxuries (30% of Wants)

Premium groceries

Upgraded tech

Gifts

Charity

Example: $360/month flexible spending

Total Wants: $1,200 (30% of take-home pay)

20% for Savings/Debt Repayment ($800 in our example)

This category builds your financial security:

Debt Payments (40% of Savings)

Credit card debt

Student loans

Personal loans

Example: $320/month extra on student loans beyond minimums

Emergency Fund (30% of Savings)

Savings account for unexpected expenses

Example: $240/month until reaching 3-6 months of expenses

Retirement (20% of Savings)

401(k) beyond any employer match

IRA contributions

Example: $160/month into Roth IRA

Investments (10% of Savings)

Brokerage accounts

Other investments

Example: $80/month into index funds

Total Savings: $800 (20% of take-home pay)

Adjusting the Percentages

While 50-30-20 is a good starting point, you may need to adjust based on:

High cost-of-living areas: May require 60% to Needs

Aggressive debt payoff: Might do 50-20-30 temporarily

High earners: Could save more than 20%

Tracking Your Budget

Use tools like:

Budgeting apps (Mint, YNAB)

Spreadsheets

The envelope system (cash for categories)

Remember, the key is consistency. Even if you don't hit perfect percentages every month, using this framework will help you maintain balance between living today and securing your financial future.

🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹🌹

HOW TO MAKE AND SAVE MONEY

Financial Discipline: Key Principles for Stability and Growth

Financial discipline is the ability to manage money wisely by controlling spending, saving consistently, and making informed financial decisions. It plays a crucial role in achieving long-term financial stability and independence.

1. Budgeting and Planning

Create a monthly budget to track income and expenses.

Prioritize needs over wants to avoid unnecessary spending.

Set financial goals (short-term and long-term) to guide decisions.

2. Controlling Expenses

Avoid impulsive buying by following a spending plan.

Differentiate between essential expenses (food, rent, utilities) and luxuries.

Use the 50/30/20 rule: 50% for needs, 30% for wants, and 20% for savings/investments.

3. Saving Consistently

Follow the pay-yourself-first rule by saving before spending.

Maintain an emergency fund (3–6 months' expenses) for unexpected situations.

Use automatic transfers to savings accounts for consistency.

4. Managing Debt Wisely

Avoid unnecessary debt and prioritize paying off high-interest loans first.

Use credit cards responsibly, paying off balances in full each month.

Consider the debt snowball or avalanche method to clear debts effectively.

5. Smart Investments

Invest in assets that grow over time (stocks, mutual funds, real estate).

Diversify investments to reduce financial risk.

Understand the power of compound interest and start investing early.

6. Avoiding Financial Traps

Steer clear of get-rich-quick schemes and risky investments.

Beware of lifestyle inflation—increasing expenses as income grows.

Be mindful of peer pressure spending and focus on personal financial goals.

7. Continuous Learning and Adaptation

Educate yourself about personal finance, investments, and money management.

Adjust financial strategies based on life changes and economic conditions.

Seek professional advice when making major financial decisions.

Final Thought

Financial discipline is a habit that leads to financial freedom. By making small, smart choices daily, you build wealth, reduce stress, and secure a stable future.

👍

1